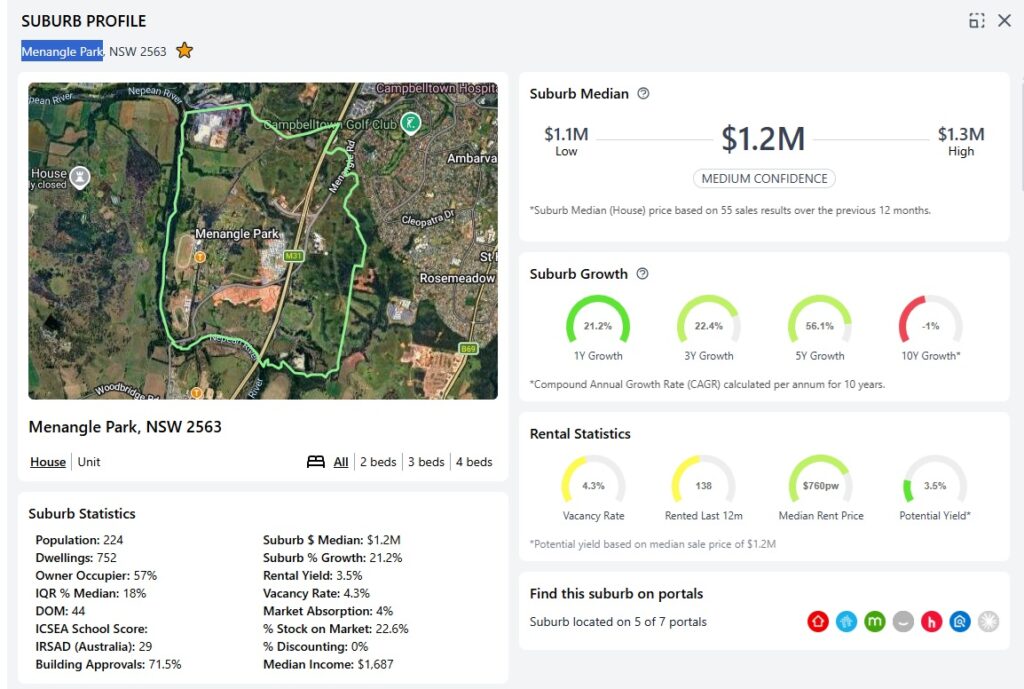

Leppington NSW Suburb Snapshot

Leppington sits in postcode 2179 inside the Camden and Liverpool local government areas, right in the middle of the South West Priority Growth Area. The suburb is home to around 9,423 residents across 4,862 dwellings, with 73 percent owner occupied. That level of owner occupation points to a settled community of families and long term buyers, alongside a steady flow of new stock coming online.

The suburb house median is around $1.24 million, with 7.4 percent price growth and a rental yield of 3.5 percent. Homes are moving at a steady pace, with 38 days on market on average, and discounting is running at 0 percent, which shows buyers are transacting at or very close to asking price.

Demand indicators remain firm. Vacancy rate sits at 2.2 percent, market absorption is 4 percent, and 11.7 percent of total stock is listed at any given time, which reflects a balanced market with real buyer choice across land only, house and land, and completed builds.

Household income sits at a median of $2,275 per week, and the interquartile ratio to median is 25 percent, pointing to a wide spread of buyer capacity across the suburb. Building approvals of 10.5 percent, an ICSEA school score of 61, and an IRSAD ranking of 89 against the national benchmark round out a suburb profile that continues to attract first home buyers, upgraders, and long term investors across the South West Sydney corridor.

Your Local Mortgage Broker in Leppington NSW

You have watched Leppington change from open fields into one of Sydney’s busiest new home suburbs, with the T5 train station, Ed Square nearby, and new estates opening every year. The next step is turning your purchase plan on land, house and land, or an established home into a loan that actually settles on time.

Laxmi Home Loans is a Mortgage Broker Leppington families rely on for home loans, construction finance, refinance, and investment loans. We have supported buyers across South West Sydney since 2015, with more than 1,000 Australian families settled and over 400 five star reviews on public platforms.

Leppington NSW Suburb Snapshot

Leppington sits in postcode 2179 inside the Camden and Liverpool local government areas, right in the middle of the South West Priority Growth Area. The suburb is close to the future Western Sydney International Airport at Badgerys Creek, the Leppington train station on the T5 line, new schools, and a fast growing network of shops and parks.

Most Leppington homes are new builds on freshly registered land, spread across a mix of established pockets and greenfield release areas. That mix of land only, house and land, and completed builds means buyers have real choice, but it also means loan structure needs to be matched to the type of purchase.

Why Leppington is a Unique Market for a Home Loan Broker

Leppington sits at the meeting point of two growth stories, the T5 rail corridor moving south from Edmondson Park, and the airport catchment moving west through Austral and Bringelly. Each side of the suburb attracts a slightly different buyer profile, from first home buyers targeting the train line to investors chasing land value growth near the airport.

Loan structure matters more here than in an older suburb, because the same purchase price can involve very different loan setups depending on whether you buy a finished home, take a house and land package, or purchase land first and build later. Getting the wrong structure at the start can cost you months at settlement and thousands in unnecessary interest during the build.

Home Loan Broker Leppington NSW for Local Buyers

Most buyers in Leppington fall into one of four groups, first home buyers stepping into their first property, growing families upgrading from a townhouse or apartment, investors targeting land value growth in the airport catchment, or refinancers who bought in the early 2020s and want a sharper deal. A well matched home loan strategy starts with lining up your goal, your income, and the right lender on our panel of more than 50 banks and non bank lenders.

We work through your deposit position, existing debts, family plans, and future income before we recommend any structure. That way the loan you settle today still fits you in five, ten, or twenty years, not only in the first twelve months.

First Home Buyer Loans Leppington NSW

Leppington is one of the most active first home buyer suburbs in Sydney because of the volume of new housing and access to government support. Eligible buyers can look at the First Home Guarantee, which allows a 5 percent deposit with no lenders mortgage insurance, and the New South Wales First Home Buyer Assistance Scheme, which reduces or removes stamp duty within set price caps.

Our team helps you check eligibility, prepare payslips, savings history, and evidence of genuine savings, and pre position your file so the lender sees a strong applicant, not just a strong salary. Start with our first home buyer service or the first home buyer quiz to see where you stand.

Construction Loan Leppington for House and Land Buyers

A large share of Leppington stock is either new build or freshly registered land inside estates such as Willowdale and the surrounding release areas of Austral, Bringelly, and Denham Court. A Construction Loan Leppington lender releases funds in stages, called progress payments, as the builder finishes each part of the build.

You only pay interest on the amount drawn at each stage, which keeps your holding costs manageable during construction. We help you compare fixed price builder contracts, land settlement dates, progress payment schedules, and the right construction loan structure so you are not caught out by long build times, holding costs, or a shortfall at final draw.

Investment Loan Leppington and the South West Growth Corridor

Leppington, along with Austral, Edmondson Park, and Oran Park, has been one of Sydney’s most active investor pockets for the past decade. Land supply, transport upgrades, and the future Western Sydney Airport make it a common entry point for property investors, especially those building a portfolio close to home.

We help investors compare interest only versus principal and interest, offset versus redraw, and equity release strategies from an existing property. Read more on our investment property loan page and our guide on offset account versus redraw, and see how the proposed negative gearing and CGT changes may affect future strategy. We do not give tax advice and refer you to a registered tax agent for that side.

Refinance Leppington Home Loans

If you bought or built in Leppington during 2020 to 2023, your loan may be sitting at a rate higher than what your current income, equity, and repayment history could qualify for today. A structured refinance review checks whether a rate change, a cashback offer, or a full switch of lender genuinely leaves you better off after fees.

Our refinance service looks at three scenarios, staying put with a repricing request, moving to a sharper lender, and restructuring to release equity for renovations or an investment property. You can also start with our refinance feasibility calculator.

Specialist Lender Policies Available Through Our Mortgage Broker Leppington Service

Different lenders on our panel run different specialist policies for different professions, employment types, and life stages. As your Mortgage Broker Leppington team, we match your file to the policy that gives you the strongest possible outcome. The following overview shows some of the specialist policies we can access on your behalf, subject to eligibility and lender credit approval.

Medical Professional LMI Waivers on a Leppington Home Loan

Eligible medical professionals may borrow up to 95 percent LVR with no lenders mortgage insurance under selected lender policies, with a maximum loan amount of $5 million and total lending capacity of up to $7.5 million with the LMI waiver applied. Professional qualifications are verified as part of the application.

Occupations eligible for the 95 percent LVR LMI waiver with no minimum income requirement include Dentists, General Practitioners, Medical Specialists, and hospital employed Doctors including Interns, Residents, Registrars, and Staff Specialists. Occupations eligible for a 90 percent LVR LMI waiver with a minimum income of $90,000 per annum include Audiologists, Chiropractors, Midwives, Occupational Therapists, Osteopaths, Physiotherapists, Podiatrists, Psychologists, Radiographers, Registered Nurses, Sonographers, Speech Pathologists, Optometrists, Pharmacists, and Veterinary Practitioners.

Accounting and Legal Industry LMI Waivers

Applicants working in accounting or legal roles may borrow up to 90 percent LVR with no lenders mortgage insurance under industry specialisation policies. Eligibility depends on approved industry accreditation, income requirements, and lender credit assessment.

Self Employed Income Verification Options

Self employed applicants can be assessed under a Fast Track method by providing their latest two years of individual ATO Notice of Assessment for borrowing up to 80 percent LVR. Eligible medical professionals may still access the medico LMI waiver of up to 95 percent LVR alongside self employed income verification, and non Fast Track applications can be assessed using latest year income for eligible applicants who meet the criteria.

Emergency Services Income Policy

Eligible frontline emergency services employees can have their overtime and allowances assessed at 100 percent under certain lender policies. Eligible professions include Fire Officers, Firefighters, Police Officers, Ambulance Officers, Paramedics, and hospital employed Nurses, Doctors, Surgeons, and Specialists.

Casual Teachers and School Staff Income

Income for casual teachers and other school staff can be annualised over 48 weeks with a single year to date payslip covering a minimum of three months of casual income. Further options are available where a longer income history is needed.

Construction Loan Policy Highlights

Construction loan options include variable and fixed rate loans for both owner occupied and investment purchases, with a maximum LVR of 95 percent for Owner Occupier and 90 percent for Investor inclusive of LMI, or up to 80 percent LVR without LMI. Cash out of up to $250,000 for renovations to an existing property can be arranged without progress draws using an as is valuation, under non LMI lending.

The First Home Owner Grant can be released at land settlement for eligible buyers purchasing or refinancing land and construction together, provided grant approval is in place. We encourage clients to seek independent tax advice on grant treatment.

Parental Leave Support Options

Selected lenders support parents by allowing paused repayments or a switch to interest only during the parental leave period, reduced repayments by up to 50 percent for up to six months, or use of excess payment funds to pause or reduce repayments for a set period. Return to work income can also be considered as part of your borrowing power assessment.

Note that interest continues to accrue on the loan balance during any pause or reduction in repayments.

Priority Refinance and Equity Access

A Priority Refinance option lets certain refinances progress without waiting for the outgoing lender to complete a discharge, which can save weeks on the settlement timeline. For mortgage insured loans, eligible clients can also request up to $100,000 in equity for renovation, personal, or investment purposes.

First Home Buyer Family Security Guarantee

The Family Security Guarantee allows a family member to support a first home buyer or investor without a serviceability assessment on the guarantor, subject to policy conditions. Applicants and family members are encouraged to seek independent legal advice and understand the risks and exclusions associated with guarantee arrangements before proceeding.

Next Home Buyer Portability and Bridging Finance

Portability lets an existing home owner switch the security on a loan without changes to the loan details or a new serviceability assessment. Bridging Interest Capitalised finance is also available, with servicing assessed on the end debt where applicable and a bridging facility that can remain in place for up to 12 months.

For clients close to retirement, projected superannuation using the ASIC MoneySmart Superannuation Calculator can be used to support an exit strategy where the loan term extends past standard retirement age.

Investor Features Including Interest in Advance

Investors may access an additional interest rate discount for paying 12 months of interest up front under an Interest in Advance option. Investment loans can also be structured up to 90 percent LVR with interest only repayments inclusive of LMI, and a negative gearing calculator is available for on the spot serviceability projections.

Upfront Valuations

A property valuation can be ordered before a formal loan application in some cases, giving both you and us confidence on borrowing capacity before contracts are signed. Some policy conditions apply.

Note that the LVR figures above refer to the initial loan to value ratio at settlement, and home loan rates for new loans are set based on the initial LVR and do not change over the life of the loan as the LVR changes.

Leppington Home Loans for Every Client Type

Leppington is home to a wide mix of professionals, tradies, healthcare workers, business owners, and new migrants. We hold specialist experience with the following borrower types, and we match your file to the lenders who treat your income and profession the way they should.

- Registered Nurses and Midwives, with access to LMI waiver options for eligible healthcare professionals, up to 90 percent LVR on selected lenders

- Doctors, Dentists, Accountants, and Legal professionals, with LMI waivers up to 95 percent LVR on selected lenders

- PAYG employees on permanent, part time, or long term casual employment

- Self employed and sole traders using one year or two year financials

- SMSF trustees looking at an SMSF property loan

- Visa holders including 482, 485, 186, 189, 190, and partner visa applicants

- Guarantor loans where parents help their children into their first home

- Bridging finance for buyers who need to purchase before selling

Nepali Speaking Mortgage Broker Serving Leppington

Leppington sits inside a tight cluster of growing suburbs we work with every week. If you are looking at nearby areas as well, you can compare our local pages for Liverpool, Camden, Campbelltown, and Fairfield.

Many of our clients search for a Home Loan Broker Leppington or a Nepali Mortgage Broker in Leppington before finding us, because we serve the same catchment through the Liverpool and Camden corridor. Our office supports clients in English, Nepali, and Hindi, so families who prefer a Nepali speaking mortgage broker can walk through their file in the language they are most confident in.

What Our Leppington Clients Say

“I highly recommend Kishor from Laxmi Home Loans. He is a Nepali mortgage broker who helped us buy our first home.”

Reviews like this sit alongside our RateMyAgent National Top 20 Customer Service ranking for 2025 and 2026, MFAA Full Membership, and Local Business Awards recognition in the Cumberland region. Track record matters when you are placing your family’s biggest financial decision in someone else’s hands.

How Our Leppington Home Loan Process Works

- Book a free consultation with our team, in person, online, or over the phone

- Share your income, savings, debts, and goals so we can map your borrowing capacity

- We compare lender policies across our 50 plus panel and shortlist the top three options

- You choose the loan that fits your goals and we lodge the application on your behalf

- We follow the file through valuation, formal approval, and settlement

- After settlement, we review your loan every 12 to 18 months so it keeps working for you

Frequently Asked Questions

How much deposit do I need for a Mortgage Broker Leppington application?

Most lenders look for at least 5 percent of the purchase price plus government and legal costs, and this is where the First Home Guarantee helps. Genuine savings history over three months is usually required, along with evidence of employment and living expenses.

Can a First Home Buyer use the First Home Guarantee in Leppington?

Yes, eligible first home buyers can use the First Home Guarantee within the current Sydney price cap and buy with a 5 percent deposit without lenders mortgage insurance. Eligibility depends on your income, citizenship or permanent residency status, and property price.

How does a Construction Loan Leppington work for house and land buyers?

Land settles first, then the lender releases funds in stages to the builder as work is completed, usually across five progress payments. You only pay interest on the drawn balance during construction, and the loan converts to a standard home loan after handover.

Can a Registered Nurse get an LMI waiver on a Leppington home loan?

Yes, eligible healthcare professionals including Registered Nurses and Midwives can access LMI waivers up to 90 percent LVR with selected lenders, subject to a minimum income threshold. Eligibility depends on income, employment status, and registration with the relevant professional body.

Can visa holders use a Home Loan Broker Leppington service?

Yes, several lenders on our panel accept applicants on temporary skilled visas including the 482 and 485, subject to FIRB rules, deposit size, and income evidence. We match your visa type to lenders who treat that visa fairly, so you do not waste an application on the wrong bank.

Does your Mortgage Broker Leppington service cover other Sydney suburbs?

Yes, we are based in Merrylands and serve clients Australia wide, with a strong local footprint across Leppington, Austral, Edmondson Park, Bringelly, Denham Court, Liverpool, Camden, Campbelltown, and the wider Cumberland region. Meetings can be in person, by video, or over the phone.

For a wider list of common questions across home loans, refinance, construction, and investment finance, visit our full Home Loan FAQs Australia page.

Ready to Discuss

Whether you are buying land, buying a completed home, building your first place, refinancing an existing loan, or adding an investment property, our team is happy to walk you through your options with no pressure and no obligation. Call 0433 589 626 or 1300 4 LAXMI, email [email protected], or use our free consultation booking page. You can also head to our contact page or the Laxmi Home Loans homepage for more.

This content is general in nature and does not consider your personal financial situation. All loan approvals are subject to lender credit assessment, eligibility criteria, and terms and conditions.

By Kishor Acharya and LHL Team