Government schemes for first home buyers in Australia can help eligible buyers enter the property market sooner by reducing deposit pressure, lowering upfront costs, and helping some borrowers avoid Lenders Mortgage Insurance. Federal support such as the Australian Government 5% Deposit Scheme can allow eligible buyers to purchase with a deposit as low as 5 percent, while eligible single parents or single legal guardians may be able to buy with a minimum 2 percent deposit through the single parent pathway.

State and territory programs can also support first home buyers through First Home Owner Grants, stamp duty exemptions, and transfer duty concessions. These programs vary depending on where the property is located, the purchase price, the property type, and the buyer’s eligibility. With the right home loan specialist, first home buyers can understand which schemes apply, compare participating lenders, and structure their application with confidence.

Key Takeaways

- Eligible first home buyers may be able to buy with a 5 percent deposit and avoid Lenders Mortgage Insurance through the Australian Government 5% Deposit Scheme.

- Eligible single parents or single legal guardians may be able to purchase with a minimum 2 percent deposit, subject to scheme and lender criteria.

- First Home Owner Grants are generally state or territory based and often apply to new homes, newly built homes, or substantially renovated properties.

- Stamp duty exemption first home buyer schemes can reduce one of the largest upfront costs when purchasing a property.

- Federal and state schemes may be combined in many cases, but eligibility depends on the buyer, property type, purchase price, location, lender policy, and current government rules.

1. Why Government Schemes Matter for First Home Buyers in Australia

Buying your first home in Australia can feel exciting, but it can also feel financially challenging. Many first home buyers have stable income and good savings habits, yet still struggle to build a large enough deposit while paying rent, bills, transport, groceries, family expenses, and everyday living costs.

For many buyers, the biggest barrier is not always the monthly home loan repayment. The bigger challenge is saving enough money upfront. A traditional home loan usually becomes easier to access when a buyer has a 20 percent deposit, because this can help avoid Lenders Mortgage Insurance. However, saving 20 percent of a property price can take years, especially in markets such as Sydney, Melbourne, Brisbane, Perth, Adelaide, Canberra, and major regional centres.

Government schemes for first home buyers in Australia are designed to reduce some of these barriers. These schemes may help eligible buyers purchase with a smaller deposit, reduce or remove Lenders Mortgage Insurance, access a First Home Owner Grant, or save money through stamp duty exemptions and concessions.

For example, a first home buyer may have saved a 5 percent deposit and believe they need to wait several more years before applying for a loan. If they meet the relevant criteria, the Australian Government 5% Deposit Scheme may allow them to buy with a smaller deposit and avoid Lenders Mortgage Insurance through a government guarantee. Housing Australia states that eligible first home buyers can access the scheme through participating lenders, subject to price caps and lender approval.

This can make a real difference. A buyer purchasing a $700,000 home would usually need $140,000 for a 20 percent deposit. A 5 percent deposit would be $35,000. That difference can change how soon a buyer enters the property market.

However, a smaller deposit also means a larger loan. This is why first home buyers should look beyond eligibility and consider affordability. A government scheme can help reduce upfront costs, but the loan still needs to suit the buyer’s income, expenses, family situation, and long-term goals.

This is where working with a home loan specialist becomes valuable. A mortgage broker can help first home buyers understand the difference between scheme eligibility and loan approval. They can also compare lenders, check genuine savings requirements, review property price caps, calculate borrowing capacity, and explain the total funds needed at settlement.

At Laxmi Home Loans, first home buyers often ask questions such as:

Can I buy my first home with a 5 percent deposit in Australia?

Can I avoid Lenders Mortgage Insurance as a first home buyer?

Can I combine the First Home Guarantee and a state grant?

Do I qualify for the first home owner grant NSW?

Which stamp duty exemption first home buyer options apply to me?

These are important questions because every buyer’s situation is different. The right answer depends on the property location, purchase price, income, deposit, residency status, family situation, lender policy, and government scheme rules.

For first home buyers, the best outcome usually comes from combining the right scheme, the right lender, and the right loan structure.

2. Federal Government Schemes for First Home Buyers

The main federal support for eligible first home buyers is delivered through Housing Australia and participating lenders. The Australian Government 5% Deposit Scheme is designed to help eligible buyers purchase sooner by reducing the deposit barrier and helping them avoid Lenders Mortgage Insurance.

Under this scheme, eligible first home buyers may be able to purchase with a deposit as low as 5 percent. The government provides a guarantee to the lender, which helps eligible borrowers avoid LMI. This guarantee does not mean the government gives the buyer cash, and it does not mean the government pays part of the loan. It means the government supports part of the loan risk for the lender.

For first home buyers, this can be a major advantage. Lenders Mortgage Insurance can add thousands of dollars to the cost of buying a property. It protects the lender, not the borrower, if the borrower defaults and the lender suffers a loss. Avoiding LMI can reduce the cost of entering the market and help buyers use their savings more effectively.

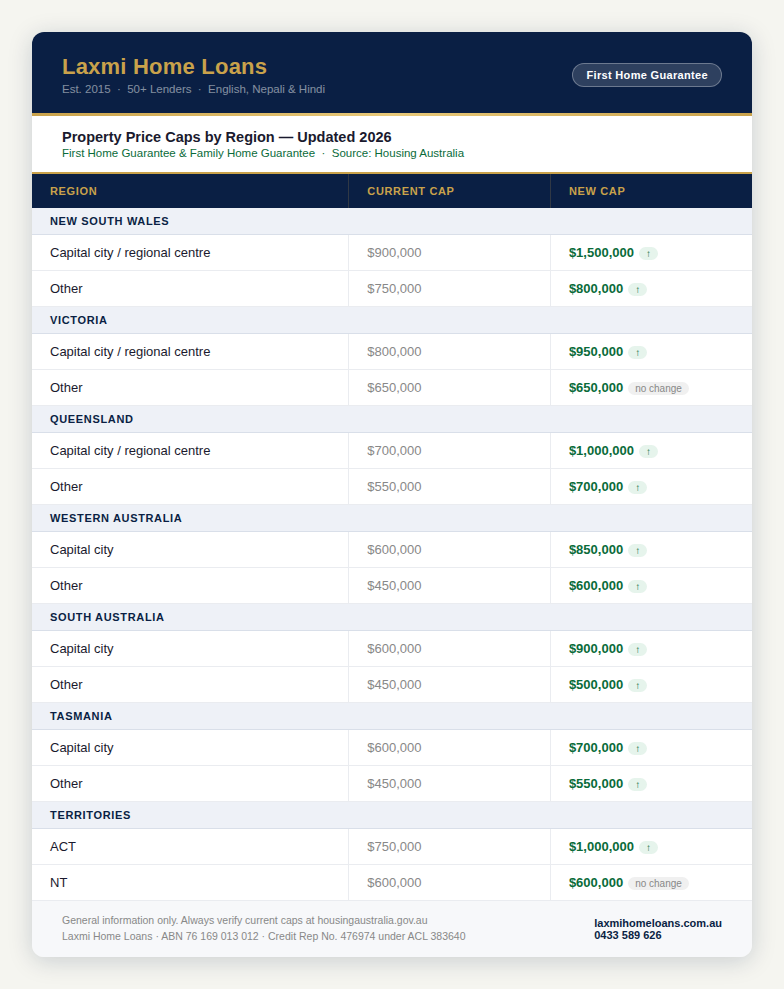

Housing Australia also applies property price caps under the scheme. These caps vary by state, territory, capital city, regional centre, and other areas. Housing Australia provides a property price cap tool and states that both the purchase price and the lender-assessed value must be at or below the relevant cap.

From 1 October 2025, Housing Australia announced an expansion of the scheme, including higher property price caps, no place limits, and no income caps for first home buyers under the expanded Home Guarantee Scheme settings. Buyers should always confirm the current rules at the time of application because government policy and lender participation can change.

Another important pathway is support for eligible single parents and single legal guardians. Housing Australia states that eligible single parents or single legal guardians with one or more dependent children may be able to buy with a minimum 2 percent deposit and no LMI through the scheme, subject to eligibility and lender approval.

This can be especially helpful for single-income households. A single parent may be managing rent, childcare, school expenses, groceries, transport, and other household costs while trying to save for a deposit. A 2 percent deposit option may make home ownership more realistic, provided the loan remains affordable.

To access federal government backed home loan schemes for first home buyers Australia-wide, buyers generally need to meet scheme criteria, buy an eligible property, purchase within the relevant price cap, live in the home as an owner-occupier, and apply through a participating lender. The borrower must also meet the lender’s normal credit and serviceability requirements.

This is an important distinction. A buyer may qualify for the scheme but still need to prove to the lender that the loan is affordable. The lender will assess income, expenses, debts, credit cards, personal loans, employment history, savings conduct, dependants, and credit history.

A home loan specialist can help match the buyer to a lender that suits their profile. This matters because participating lenders may assess borrowers differently. One lender may be more suitable for a salaried employee, while another may be stronger for self-employed income, family gifted deposits, overtime income, or applicants with complex circumstances.

At Laxmi Home Loans, the goal is to help first home buyers understand not only which government schemes may apply, but also which lender may support the application properly.

3. First Home Owner Grants and Stamp Duty Support by State

Federal schemes can reduce deposit and LMI pressure, but state and territory support can reduce other upfront costs. These programs usually include First Home Owner Grants, stamp duty exemptions, transfer duty concessions, and other home buyer assistance schemes.

The exact support available depends on the state or territory where the property is located. This is why first home buyer grants by state Australia can vary significantly.

In New South Wales, first home buyers may be eligible for the First Home Buyers Assistance Scheme. Revenue NSW states that from 1 July 2023, eligible first home buyers may receive a full transfer duty exemption for new or existing homes valued up to $800,000, while homes valued over $800,000 and less than $1,000,000 may qualify for a concessional rate. Revenue NSW also provides information about the First Home Owner Grant for newly built or substantially renovated homes.

This is important because stamp duty can be one of the largest upfront costs in a property purchase. A stamp duty exemption first home buyer benefit can reduce the amount needed at settlement and make the purchase more achievable.

For example, a first home buyer in NSW purchasing an eligible home under the exemption threshold may save a significant amount in transfer duty. If they are buying a new home, they may also need to check whether the first home owner grant NSW applies to their property.

Victoria also provides first home buyer support through the State Revenue Office Victoria. The SRO explains that eligible buyers can apply for the First Home Owner Grant through an approved agent such as a bank or credit union, or directly in certain circumstances.

Other states and territories, including Queensland, South Australia, Western Australia, Tasmania, the Australian Capital Territory, and the Northern Territory, have their own first home buyer programs. Some offer grants for new homes. Some offer stamp duty concessions. Some apply different thresholds depending on whether the buyer is purchasing a house, apartment, vacant land, house and land package, or off-the-plan property.

The key point is that first home buyers should not assume that one state’s rules apply everywhere. A buyer in Sydney may have different options from a buyer in Melbourne, Brisbane, Perth, Adelaide, Hobart, Darwin, Canberra, or a regional area.

A common misunderstanding is that every first home buyer receives a cash grant. In many cases, First Home Owner Grants apply only to new homes, newly built homes, substantially renovated homes, or house and land packages. Established homes may not qualify for a grant in many states, although they may still qualify for stamp duty relief depending on local rules.

Another common misunderstanding is that stamp duty support is automatic. Buyers usually need to meet eligibility criteria, purchase under the relevant threshold, satisfy residency requirements, and provide the required documents.

For couples, previous property ownership can also affect eligibility. If one applicant or their spouse has previously owned residential property in Australia, this may affect access to certain schemes.

This is where expert guidance can prevent costly mistakes. If a buyer assumes they will receive a grant or exemption and later discovers they do not qualify, their funds to complete may fall short. That can create stress close to settlement.

A home loan specialist can help first home buyers understand:

- Whether the property type is eligible

- Whether the purchase price is within the threshold

- Whether stamp duty relief applies

- Whether a First Home Owner Grant applies

- Whether the grant is available at settlement or after settlement

- Whether the lender can process the grant application

- Whether the buyer has enough funds to complete the purchase

At Laxmi Home Loans, this review is part of helping first home buyers prepare properly before they commit to a property.

4. Can You Combine the First Home Guarantee and State Grants?

Many buyers ask whether they can combine the First Home Guarantee and state grant support. In many cases, federal and state schemes may work together because they support different parts of the home buying process.

The First Home Guarantee Australia pathway can help eligible buyers purchase with a smaller deposit and avoid LMI. A state First Home Owner Grant may provide cash support for an eligible new home. A stamp duty exemption or concession may reduce the amount payable at settlement.

For example, a first home buyer purchasing a new eligible property may be able to use a 5 percent deposit scheme, avoid LMI, apply for a First Home Owner Grant, and receive stamp duty relief if the property is under the relevant threshold. The final outcome depends on the property, location, purchase price, buyer eligibility, and lender policy.

In NSW, Revenue NSW confirms that eligible first home buyers may receive transfer duty assistance for new or existing homes within the relevant thresholds. Revenue NSW also lists the First Home Owner Grant as a separate program for newly built or substantially renovated homes. This means a buyer may need to assess both duty assistance and grant eligibility separately.

Here is a practical example.

A first home buyer wants to purchase a newly built townhouse. The buyer has saved a 5 percent deposit, the property is within the Housing Australia price cap, and the buyer meets the federal scheme criteria. If the property also meets state grant rules and falls within the stamp duty concession threshold, the buyer may benefit from multiple forms of support.

Now consider a different example.

A first home buyer wants to purchase an established apartment. The property may still qualify for the federal 5 percent deposit scheme if it meets the price cap and scheme rules. The buyer may also qualify for stamp duty relief depending on the state. However, they may not qualify for a First Home Owner Grant if that grant is limited to new homes.

This is why the question “Can I combine First Home Guarantee and state grant?” depends on the actual property and buyer profile.

Buyers should also understand that combining schemes does not guarantee loan approval. The lender still needs to assess whether the borrower can afford the loan. The lender will review income, employment, expenses, debts, repayment history, credit score, deposit source, and property details.

Another important factor is funds to complete. A buyer may have a 5 percent deposit, but still need money for legal fees, bank fees, government charges, inspections, moving costs, insurance, and any remaining stamp duty. If a grant is paid after settlement rather than at settlement, the buyer may need extra funds upfront.

Genuine savings can also affect loan approval. Some lenders want to see that the buyer has saved a portion of the deposit over time. Gifted deposits, family support, bonuses, and grants may be acceptable with some lenders, but policies differ.

A first home buyer no LMI loan can be a powerful option, but it should be structured carefully. The repayment must be comfortable, not just technically approved. A larger loan may mean higher repayments and more interest over time.

At Laxmi Home Loans, the approach is to check both opportunity and risk. The team helps buyers understand what support may apply, what costs still remain, which lenders may suit the application, and whether the repayment fits the buyer’s lifestyle.

GET IN TOUCH

Ready to check your eligibility and compare lenders?

5. How to Buy Your First Home with a 5 Percent Deposit in Australia

Many first home buyers search for how to buy first home with 5 percent deposit Australia because saving a 20 percent deposit can feel difficult. The good news is that eligible buyers may be able to purchase with a smaller deposit through the Australian Government 5% Deposit Scheme. Housing Australia confirms that the scheme can support eligible first home buyers with a minimum 5 percent deposit through participating lenders, subject to property price caps and lender approval.

The first step is understanding your deposit. A 5 percent deposit means you have saved at least 5 percent of the property purchase price. For a $700,000 property, this would be $35,000. However, the deposit is not the only cost. Buyers also need to consider legal fees, government fees, inspections, lender costs, moving costs, insurance, and any stamp duty that still applies.

The second step is checking the property price cap. Housing Australia states that the purchase price and lender-assessed value must be at or below the applicable price cap. If the property is above the cap, the scheme may not apply.

The third step is checking loan affordability. A smaller deposit usually means a larger loan. A larger loan can mean higher repayments. Before buying, first home buyers should understand how repayments may change if interest rates move, living costs increase, or personal circumstances change.

The fourth step is choosing a participating lender. Not every lender may be suitable for every borrower. A buyer with PAYG income, self-employed income, family gifted deposit, overtime, commission, or recently changed employment may need a lender with the right policy.

The fifth step is preparing documents. First home buyers usually need identification, payslips, bank statements, savings records, rental history, tax documents if self-employed, and details of existing debts. Preparing these documents early can help the loan process move more smoothly.

The sixth step is getting a borrowing capacity estimate. This helps buyers understand their realistic price range before inspecting properties. It also helps avoid disappointment from looking at homes that are outside lender or scheme limits.

The seventh step is checking state support. A buyer using a 5 percent deposit scheme may also qualify for a state grant or stamp duty concession, depending on the property and location.

The eighth step is applying for pre-approval if suitable. Pre-approval gives buyers more confidence before making an offer, although it is not final approval. Final approval depends on the property, valuation, updated documents, and lender assessment.

The ninth step is choosing the property carefully. The property should fit the buyer’s budget, lifestyle, lender criteria, and scheme rules. This includes checking whether the property is new, established, off the plan, strata, vacant land, or house and land.

The tenth step is submitting the full loan application. Once the contract is signed, the lender completes valuation, final credit assessment, scheme checks, and settlement preparation.

For first home buyers, the 5 percent deposit pathway can be helpful, but it needs to be handled correctly. The goal is not only to buy sooner. The goal is to buy confidently, with a loan that remains manageable.

A home loan specialist can help buyers avoid common mistakes such as:

- Looking at properties above the price cap

- Assuming all grants apply automatically

- Forgetting settlement costs

- Choosing a lender that does not suit their income type

- Relying on LMI waiver options without checking eligibility

- Making an offer before confirming borrowing capacity

- Underestimating repayments after settlement

At Laxmi Home Loans, first home buyers receive practical support from the early planning stage through to settlement. This includes checking scheme options, explaining lender requirements, comparing banks, reviewing documents, and helping buyers understand their full purchase budget.

6. How Laxmi Home Loans Helps First Home Buyers Choose the Right Scheme and Lender

Buying your first home is more than a loan application. It is a major financial decision that affects your lifestyle, family, savings, and future plans. Government schemes can make the journey easier, but only when they are matched with the right lender and the right loan structure.

Laxmi Home Loans helps first home buyers understand their options clearly. The team reviews the buyer’s deposit, income, employment, expenses, target location, property type, family situation, and long-term goals. This helps identify which government schemes may apply and which lenders may be suitable.

Kishor Acharya and the team at Laxmi Home Loans have helped more than one thousand families with their home loan journey. With access to over fifty banks and lenders, including lenders that may participate in federal guarantee schemes, the team can help first home buyers compare suitable options and avoid unnecessary confusion.

For many buyers, the process begins with simple questions:

How much can I borrow?

How much deposit do I need?

Can I avoid LMI?

Am I eligible for the First Home Guarantee Australia pathway?

Can I access the Family Home Guarantee or single parent support?

Do I qualify for a First Home Owner Grant?

Can I get a stamp duty exemption as a first home buyer?

Which lender is right for me?

The answers depend on the buyer’s personal situation. A first home buyer with a stable salary may have a different pathway from a self-employed buyer. A buyer using a family gift may need a different lender from a buyer with long-term genuine savings. A single parent may need a different scheme assessment from a couple buying together.

Laxmi Home Loans also supports clients from diverse communities. The team speaks English, Nepali, and Hindi, which makes the home loan process easier for clients who prefer clear communication in a familiar language. For many families, this creates comfort and trust during one of the biggest financial decisions of their life.

The team can assist with:

- First home buyer loan options

- Government scheme eligibility checks

- First Home Guarantee Australia guidance

- LMI waiver first home buyer options

- State grant and stamp duty support review

- Borrowing capacity estimates

- Participating lender comparisons

- Document preparation

- Pre-approval and loan application support

- Settlement guidance

A strong first home buyer strategy is not just about getting approved. It is about understanding the full cost, choosing a suitable loan, avoiding unnecessary risk, and making a confident decision.

If you are planning to buy your first home, you may be closer than you think. The right scheme, lender, and advice can help you move from uncertainty to a clear action plan.

Speak with Laxmi Home Loans today to explore your first home buyer options. Book a free appointment online, call 0433 589 626, or contact 1300 4 LAXMI.

Book a Free Appointment with Laxmi Home Loans

Frequently Asked Questions

Conclusion

Government schemes for first home buyers in Australia can make home ownership more achievable by reducing deposit pressure, lowering upfront costs, and helping eligible buyers avoid Lenders Mortgage Insurance. Federal support such as the First Home Guarantee Australia pathway and single parent support can help buyers enter the market sooner, while state-based First Home Owner Grants and stamp duty exemptions or concessions can reduce the amount needed at settlement.

However, every buyer’s situation is different. Eligibility depends on your income, deposit, property location, purchase price, residency status, property type, lender policy, and current government rules. A scheme may help you buy sooner, but the home loan still needs to be affordable and structured correctly.

Laxmi Home Loans helps first home buyers understand their options clearly, compare lenders, check government scheme eligibility, and prepare a stronger home loan application. Whether you want to buy with a 5 percent deposit, avoid LMI, access a state grant, or understand stamp duty exemption first home buyer options, the right guidance can make the process simpler and more confident.

To explore which government schemes you may qualify for, book a free appointment with Laxmi Home Loans, call 0433 589 626, or contact 1300 4 LAXMI. mortgage broker before making a decision. Laxmi Home Loans (Mero Chino Groups Pty Ltd T/As Laxmi Home Loans ABN: 76 169 013 012) Credit Representative No. 476974 authorised under ACL No. 383640.