Two people earning the same salary can walk into different banks and receive very different borrowing estimates. In some cases, the gap can be $100,000, $150,000, or even more than $200,000. For first home buyers in Sydney and across Australia, this can be the difference between being able to buy in a preferred suburb, needing a larger deposit, changing property type, or delaying the purchase altogether.

Borrowing power is one of the most misunderstood parts of the home loan process. Many buyers assume that if they earn a certain salary, every bank will offer a similar loan amount. In reality, banks do not calculate borrowing power from income alone. They assess your full financial position, including how stable your income is, how much tax you pay, how much you spend, whether you have dependants, how much debt you already carry, and how your application performs under a higher assessment interest rate.

In 2026, borrowing capacity remains especially important because Australian lenders continue to apply detailed serviceability checks. A lender needs to be satisfied that you can repay the proposed loan without hardship, not only at the advertised interest rate, but also under a stressed repayment scenario. That is why online borrowing calculators can be useful for a quick estimate, but they should not be treated as a final approval figure.

This guide explains how banks calculate borrowing power, why similar applicants can receive very different results, and what practical steps may help you improve your home loan borrowing capacity before applying. It is designed for first home buyers, self-employed borrowers, contractors, visa holders, and growing families who want a realistic assessment before making property decisions.

What is Borrowing Power and Why Does It Vary?

Borrowing power is the maximum loan amount a lender may be willing to approve based on your income, expenses, liabilities, credit profile, deposit, and overall risk position. It is sometimes called borrowing capacity, serviceability, or maximum loan eligibility. It is not a guaranteed approval. It is an estimate based on the lender’s calculator and lending policy at the time of assessment.

For first home buyers in Sydney and across Australia, variations in borrowing power can significantly influence key decisions. Your assessed borrowing capacity may determine whether you can purchase in your preferred suburb, how much deposit you need, what type of property you can afford, or whether you need to delay your purchase.

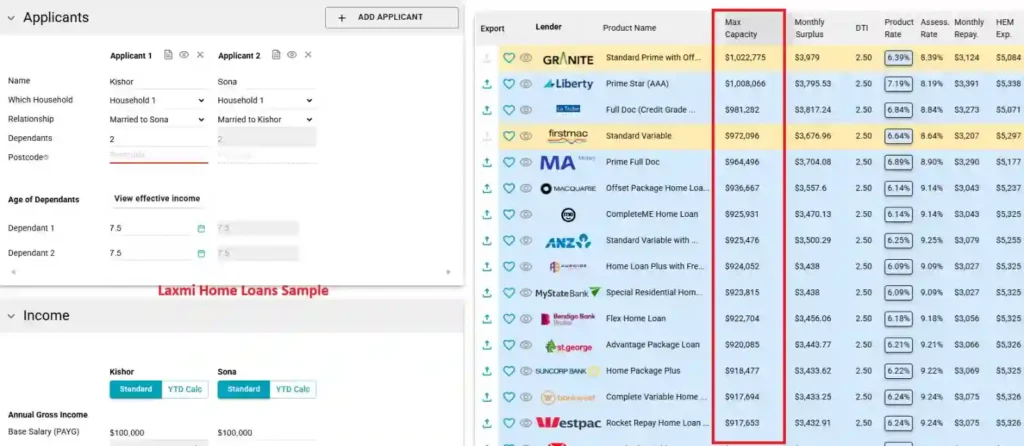

For example, consider a couple where both partners earn $100,000 annually. Depending on the lender, their borrowing capacity may vary by tens of thousands or even hundreds of thousands of dollars. As shown in the comparison below, approaching different lenders can result in substantially different estimated loan amounts.

Strategic financial adjustments, such as salary sacrificing or restructuring certain commitments, may also improve borrowing power with some banks and lenders, even if the impact is minimal with others. This is why choosing the right lender policy can be just as important as earning a strong income.

A key reason borrowing power varies is that lenders use different serviceability calculators. These calculators may look similar from the outside, but they can treat income, expenses, debts, bonuses, overtime, rental income, self-employed earnings, and credit limits differently. One bank may include 100 percent of a particular income type, while another may shade it to 80 percent, average it over two years, or exclude it altogether. One lender may be comfortable with a probationary employee in a strong industry, while another may require more employment history.

Borrowing power also changes because lenders apply policy rules differently. Some lenders are more flexible with contractors, casual workers, commission income, family tax benefits, rental income, boarder income, and applicants on temporary visas. Others may take a more conservative view. This is why a buyer who only speaks to one bank may receive a lower estimate than they could potentially obtain elsewhere.

The serviceability assessment usually begins with your gross income, but the lender then calculates what income is available after tax and regular commitments. From there, it deducts living expenses, existing loan repayments, credit card commitments, HELP or HECS repayments, child support, dependants, and other obligations. The lender then tests whether the remaining surplus is enough to cover the proposed mortgage repayment at an assessment rate.

Key Factors Banks Assess in 2026

Banks and lenders assess several interconnected factors before deciding how much you can borrow. Understanding these factors can help you prepare earlier and avoid surprises during pre-approval.

Income is the starting point. Lenders look at base salary, overtime, allowances, bonuses, commissions, rental income, self-employed income, and any other regular earnings. PAYG salary is usually the easiest income type to assess because it can be verified through payslips, bank statements, employment letters, and tax records. Variable income is assessed more carefully. Bonuses and commissions may need a track record, and lenders may average or shade them. Self-employed income is commonly assessed using business financials, tax returns, notices of assessment, and sometimes business bank statements. Some lenders may average one to two years of income, while others may use the most recent year if it is stronger and can be justified.

Expenses are equally important. Lenders compare your declared living expenses with a benchmark such as the Household Expenditure Measure, often referred to as HEM. If your declared expenses are below the benchmark that applies to your household type, the lender may use the benchmark instead. If your actual expenses are higher, the lender may use your actual figure. This means underestimating expenses does not automatically improve borrowing power. Lenders usually review bank statements and can ask questions if spending patterns do not match the application.

The interest rate buffer is another major factor. Australian Prudential Regulation Authority guidance has required regulated lenders to assess borrowers at a rate above the actual product rate. APRA confirmed in July 2025 that the mortgage serviceability buffer would remain at 3 percentage points. In practical terms, if your loan rate is around 6 percent, a regulated lender may assess your repayment capacity at around 9 percent. The purpose is to test whether you could still manage repayments if interest rates rise or your financial position changes.

Credit history and conduct also matter. Lenders assess your credit report, repayment history, defaults, hardship arrangements, personal loan conduct, credit card conduct, and the number of recent credit enquiries. A strong credit file may not automatically increase your borrowing power, but a weak credit file can reduce lender options or lead to stricter assessment.

Employment stability is another core consideration. A permanent full-time employee with several years in the same industry may be viewed differently from someone who recently changed jobs, started casual work, began contracting, or launched a business. That does not mean non-traditional employment cannot be approved. It means the right lender policy becomes more important.

Deposit size and loan-to-value ratio, or LVR, also affect the outcome. LVR compares the loan amount to the property value. A lower LVR usually means less risk for the lender, while a higher LVR may require lenders mortgage insurance and more detailed assessment. First home buyers with smaller deposits may still have options, but the approval pathway can depend on income strength, genuine savings, credit profile, and eligibility for government schemes.

Other commitments can reduce borrowing power even when they seem small. Car loans, personal loans, buy now pay later limits, credit cards, store cards, child support, private school fees, investment loan commitments, and HELP debts can all reduce the income available for a new mortgage. Credit cards are especially important because lenders may assess the limit, not just the balance. A card with a $20,000 limit can reduce capacity even if the balance is zero.

Why Two Similar Applicants Get Different Results

The most important point for first home buyers is that borrowing power is not based on salary alone. Lender calculators are policy-driven, and each lender may treat the same borrower differently. This explains why two people earning similar incomes can receive very different borrowing estimates.

Consider two applicants earning $120,000 each. Applicant A has no dependants, no credit card, no car loan, stable PAYG employment, clear savings history, and modest living expenses. Applicant B has one dependant, a $15,000 credit card limit, a car loan repayment, HELP debt, higher lifestyle spending, and income that includes irregular commissions. Even if the gross salary is the same, the lender may see Applicant A as having far more surplus income available for mortgage repayments.

The difference can become even larger when income type is assessed differently. A PAYG employee with a fixed salary may have most of their income accepted. A contractor or self-employed borrower may need to prove income through tax documents, business accounts, or consistent deposits. If one lender averages two years of self-employed income and another uses the latest year, the borrowing outcome can change substantially. If income increased recently, the wrong lender policy may hold the borrower back.

Expenses can also create a large difference. A borrower who has recently reduced spending may still be assessed on historical bank statements or a benchmark amount. A borrower with frequent discretionary spending may need to explain whether those expenses are ongoing or can be reduced after settlement. Lenders do not simply accept a lower expense figure without evidence.

Credit limits are another common reason for surprising results. Many buyers focus on their outstanding card balance, but lenders often assess the approved limit because the borrower could redraw or spend that amount in future. Closing or reducing unused credit limits before assessment may improve borrowing capacity, provided it suits the borrower’s broader financial needs.

Lender selection can also create a significant gap. Some banks are conservative with casual income, overtime, new employment, self-employed income, or visa status. Others may have stronger policies for those exact scenarios. A bank-focused approach can therefore limit options. A mortgage broker can compare a wide panel of lenders and identify which lender policy aligns with the borrower’s situation.

This is why a borrowing capacity result should be treated as lender-specific. A decline or low estimate from one lender does not always mean every lender will take the same view. It may simply mean the first lender’s policy was not the best match.

GET IN TOUCH

Ready to Know Your Real Borrowing Power?

Book your free, no-obligation consultation today and let us calculate your realistic borrowing power with access to a wide panel of lenders.

Strategies to Increase Your Borrowing Power

Improving borrowing power usually requires a combination of reducing commitments, strengthening income evidence, improving credit conduct, and choosing the right lender. The best strategy depends on your circumstances, but the following actions often make a measurable difference.

- First, reduce or close unnecessary debts where possible. Personal loans, car loans, credit cards, and buy now pay later facilities can reduce borrowing power because lenders treat them as ongoing commitments. Paying down a debt may help, but closing or reducing a credit card limit can sometimes have a stronger impact than simply clearing the balance. Before closing any facility, consider whether it affects your cash flow, emergency buffer, or broader financial plan.

- Second, build and document consistent savings. Lenders like to see that you can manage money and accumulate funds over time. A strong savings history can support your application, especially if you are a first home buyer using a smaller deposit. Genuine savings can be important for some loan types and LVR levels, and it can show that the proposed repayment will be manageable.

- Third, review your spending early. Lenders may examine recent bank statements, so waiting until the week before application is often too late. Reviewing discretionary spending three to six months before applying can help you understand what your statements show. The goal is not to hide spending. The goal is to create a sustainable budget that reflects the mortgage you want to take on.

- Fourth, structure variable income properly. If you receive bonuses, overtime, commissions, allowances, or contractor income, documentation matters. Keep payslips, employment contracts, group certificates, tax returns, invoices, and bank statements organised. Some lenders need a longer history, while others may accept a shorter track record if the income is consistent and supported.

- Fifth, check your credit report before applying. Errors, unpaid defaults, late payments, and excessive recent enquiries can create issues. Reviewing your credit file early gives you time to correct mistakes and improve conduct before seeking pre-approval.

- Sixth, consider whether a joint application is suitable. Applying with a partner or family member can increase total income, but it also adds their debts, expenses, dependants, and credit profile to the application. A joint application should be considered carefully because each borrower becomes responsible for the loan.

- Seventh, improve deposit strength where possible. A larger deposit can reduce LVR, lower lenders mortgage insurance costs, and increase lender comfort. For first home buyers, it may also be worth reviewing eligibility for relevant government schemes, grants, or concessions, depending on state, property type, income, and purchase price.

- Eighth, choose a lender whose policy fits your situation. This is where broker guidance can be valuable. A self-employed borrower, visa holder, nurse with overtime, IT contractor, investor, or first home buyer with family support may each need a different lender pathway.

For example, a self-employed contractor in Sydney may initially receive a conservative borrowing estimate because one bank averages older income figures. After a broker reviews the tax returns, identifies a stronger lender policy, reduces unnecessary credit card limits, and prepares the income evidence correctly, the borrower’s assessed capacity could improve significantly. In some real-world scenarios, changes like these can increase borrowing power by well over $100,000, although the final result depends on the lender, income, expenses, debts, and property details.

Actionable Steps to Get an Accurate Borrowing Assessment

An accurate borrowing assessment begins before you start attending open homes. If you know your realistic borrowing power early, you can search within the right price range, avoid emotional disappointment, and negotiate with more confidence.

Start by gathering your financial documents. PAYG applicants should prepare recent payslips, bank statements, identification, savings evidence, and details of debts and credit cards. Self-employed applicants should prepare personal and business tax returns, notices of assessment, business financial statements, BAS documents where relevant, and business bank statements if requested. Visa holders should have current visa details, passport information, employment evidence, and deposit source documentation ready.

Next, list every financial commitment. Include credit cards, personal loans, car loans, buy now pay later accounts, HELP debt, child support, school fees, existing mortgages, investment property costs, and any regular transfer obligations. Small commitments can have a larger effect than expected, especially when lenders annualise or stress-test them.

Then request a professional borrowing power calculation. A proper assessment should consider lender policy, not just a generic online calculator. It should test multiple scenarios, such as paying off a credit card, reducing a credit limit, adding a co-borrower, changing lender, increasing deposit, or selecting a different loan product.

After that, reduce debts where practical. If you have cash available, compare the borrowing power impact of paying down a personal loan versus keeping funds in savings. Sometimes reducing a monthly repayment improves serviceability more than increasing the deposit. The right choice depends on your numbers.

You should also seek pre-approval before making serious offers. A pre-approval is not a final loan approval, but it can give you a stronger understanding of the lender’s appetite and the documents required. Avoid submitting multiple applications directly to several banks without advice, as unnecessary credit enquiries can affect your credit file.

Finally, review and adjust your strategy. If your borrowing capacity is lower than expected, you may still have options. You might need more deposit, a different lender, fewer debts, stronger income evidence, a longer savings history, or a revised purchase price. A strategic plan can turn a disappointing first estimate into a more realistic path forward.

Summary

This guide explains how Australian banks and lenders calculate home loan borrowing power in 2026, including income, expenses, credit limits, dependants, loan-to-value ratio, employment type, credit history, and the serviceability buffer. It also explains why two first home buyers with similar salaries can receive borrowing estimates that differ by $200,000 or more. The short answer is that lenders do not assess income alone. They test how much surplus income remains after tax, living expenses, existing debts, credit card limits, HELP debts, dependants, and a higher assessment interest rate are applied. Because every lender uses its own calculator and policy settings, the same borrower can receive different results across banks. Working with a mortgage broker can help buyers compare lender policies, identify borrowing capacity blockers, and prepare a stronger application before seeking pre-approval.

Key Takeaways

- Borrowing power is not based on income alone. Lenders assess income, expenses, debts, dependants, credit conduct, deposit size, and the proposed loan repayment under a higher assessment rate.

- Two people on similar salaries can receive very different loan amounts because their debts, expenses, income type, credit limits, and lender choice may be different.

- APRA confirmed in July 2025 that the mortgage serviceability buffer for regulated lenders would remain at 3 percentage points, meaning many borrowers are assessed above their actual loan rate.

- Credit card limits, personal loans, car loans, HELP debts, child support, and buy now pay later facilities can reduce borrowing capacity even when some balances are low.

- Self-employed borrowers, contractors, visa holders, and applicants with variable income may benefit from lender policy matching because banks assess these situations differently.

- A mortgage broker can compare lender policies, identify borrowing capacity blockers, and help prepare a stronger application before formal pre-approval.

Ready to Take the Next Step with Laxmi Home Loans?

At Laxmi Home Loans, we help first home buyers, refinancers, investors, self-employed professionals, contractors, and visa holders understand their realistic borrowing power before they apply. Instead of relying on one bank’s calculator, our team can compare options across a wide lender panel and identify policies that may suit your income type, deposit position, credit profile, and long-term goals.

For many buyers, the most valuable part of the process is clarity. We explain what lenders are likely to assess, what may be reducing your borrowing capacity, and what steps may improve your position. This can include reviewing credit card limits, existing debts, savings history, income documents, self-employed tax returns, and potential lender choices.

Laxmi Home Loans provides multilingual support in English, Nepali, and Hindi, helping clients across Australia understand the home loan process with clear communication. Our service is especially helpful for first home buyers and migrant families who want practical guidance from initial borrowing capacity review through to pre-approval and settlement.

Book a free, no-obligation consultation or request a callback today. We can calculate your realistic borrowing power, explain your lender options, and develop a tailored strategy to help you move closer to home ownership.

Book a free consultation with Laxmi Home Loans today and find out what your LVR means for your home buying plan.

Frequently Asked Questions

Disclaimer

This article provides general information only and does not constitute financial, legal or tax advice. Lending policies, government scheme rules, eligibility criteria, property price caps and interest rates can change, so always verify your personal situation with a qualified mortgage broker, participating lender or relevant government source before making a decision.