A low bank valuation does not always mean you have paid too much. Learn why valuations come in lower, what it means for your home loan, and how Laxmi Home Loans helps clients find practical solutions.

Bank Valuation Came in Lower Than Your Purchase Price? Here Is What You Can Do

By Kishor Acharya and LHL Team

Hearing that your bank valuation has come in below your purchase price is one of the most stressful moments in a home loan application. Many buyers assume this means they have overpaid, but that is often not the case.

You may find yourself asking whether you paid too much, whether your loan will be declined, or whether you need a bigger deposit. A low valuation does not automatically stop your loan from proceeding.

At Laxmi Home Loans, we regularly help clients work through valuation shortfalls. This article explains why valuations can come in lower, what it means for your loan, and what you can do next.

What Is a Bank Valuation

When you apply for a home loan, the lender orders an independent valuation of the property. The valuer works for neither you nor the seller, and their job is to estimate the current market value based on the evidence available at the time of inspection.

Lenders use this figure to manage their own lending risk. They want to know what the property is worth today, not necessarily what you agreed to pay for it.

Why Does a Valuation Come in Lower

Many buyers assume a low valuation means they paid too much. That is not always true, and there are several common reasons behind the gap.

The Market Has Changed

Property markets move up and down between the day you sign a contract and the day the valuation is completed. If prices soften in the meantime, the valuation can land below your contract price even though nothing was wrong with your original offer.

This becomes more common when interest rates rise, buyer demand slows, more properties come onto the market, government policy changes affect borrowing capacity, or a developer releases a large number of similar lots at once.

The Valuer Uses Different Comparable Sales

Every valuation relies heavily on comparable sales. One valuer may select different comparable properties than another, and two experienced valuers can reach different conclusions while both following professional standards.

This is part of the reason valuations can vary between lenders on the very same property.

Construction Valuation Issues

Construction loans are more complex to value, because the valuer must assess the land, the building contract, floor area, specifications, inclusions, quality of construction, and location together. If any of that information is misunderstood or overlooked, the final figure can come in incorrectly.

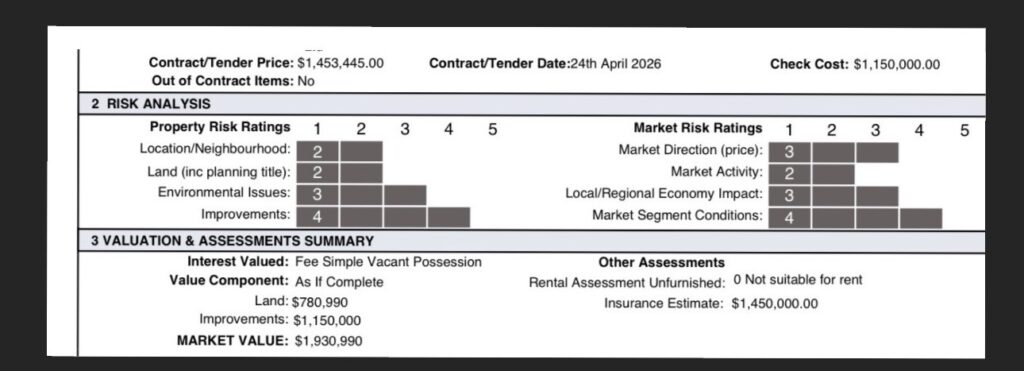

We recently assisted a client building a new home where the valuation came back well below the combined land and construction contract price. After reviewing the report, we found that the valuer had misunderstood the builder’s tender and had left out several construction components.

We contacted the valuer with clarification, but the report was not revised. Rather than treat the deal as over, we moved the application to other suitable lenders, who ordered their own independent valuations.

Both new valuations supported the full contract price, and the loan proceeded. Sometimes the issue is not the property. It is simply the valuation methodology used by one particular lender.

Can Different Banks Get Different Valuations

Yes, and this surprises many buyers. Every lender works with different valuation panels, different valuation companies, different risk policies, and different lending guidelines.

One lender may order a conservative valuation while another assesses the same property right at the contract price. This happens more often than most people realise.

Does a Low Valuation Mean the Property Is Worth Less

Not necessarily. A valuation is one professional opinion based on the evidence available at a specific point in time, and it is not an exact science.

Different valuers can interpret the same market in different ways.

What Happens If the Valuation Is Lower

The outcome depends on how far the valuation sits below your purchase price. As an example, if you agree to pay $800,000 for a property and the bank valuation comes back at $760,000, the lender will usually lend against the lower figure rather than the purchase price.

This can affect your loan to value ratio and may mean you need a larger deposit, a guarantor, a different lender, or a revised loan structure. Every situation is assessed on its own facts.

What Can Be Done

Many buyers assume there is no solution once a low valuation comes back. In reality, there are usually several options worth exploring.

Review the Valuation

We carefully review the report for factual errors, missing improvements, incorrect land size, incorrect building specifications, or missing comparable sales. Where appropriate, these points can be raised with the lender.

Seek Clarification

If genuine information has been overlooked, we can provide additional supporting evidence to the valuer. Valuers are independent and will not always amend their report, but it is always worth checking whether a factual error has affected the outcome.

Consider Another Lender

Not every lender uses the same valuation provider. A different lender may use another valuation firm, apply different lending policies, and reach a different outcome for the same property. This is often one of the most effective solutions available.

Review the Loan Structure

Sometimes adjusting the loan structure resolves the shortfall, whether that means increasing the deposit, drawing on genuine savings, including a guarantor, or adjusting the construction budget where appropriate. The right approach depends entirely on your circumstances.

Why Choosing the Right Mortgage Broker Matters

A broker does far more than compare interest rates. When an unexpected valuation issue arises, experience in reading the report and knowing which lenders to approach next becomes valuable.

At Laxmi Home Loans, we work with more than 50 banks and lenders across Australia. If one lender’s valuation creates difficulty, we assess whether another lender is likely to be more suitable based on your circumstances and their lending policy. If you are weighing up your options, our article on using a broker versus going direct to a bank explains the difference in more detail, and our list of questions to ask a mortgage broker can help you compare your options with confidence.

Important Things to Remember

A low valuation does not always mean you overpaid.

Property values change over time, sometimes between contract signing and valuation.

Different banks can produce different valuation results for the same property.

Construction valuations can sometimes contain factual misunderstandings.

There are often practical solutions available before you give up on a purchase.

Frequently Asked Questions

Can I challenge a bank valuation?

Yes, but only where there is evidence of factual errors, missing information or inappropriate comparable sales. The bank decides whether the valuer will review the report.

Can another bank order a different valuation?

Yes. Different lenders often use different valuation firms and may receive different valuation outcomes for the same property.

Will my loan be declined if the valuation is low?

Not always. Many low valuation cases can still proceed by restructuring the loan or moving the application to another lender.

Should I cancel my contract if the valuation is low?

Not necessarily. Speak with an experienced mortgage broker before making any decision, so you understand every option available to you.

Final Thoughts

A low valuation can feel overwhelming, but it does not always mean your purchase is over. Every valuation tells one story based on one lender’s assessment at one point in time.

With the right advice and access to multiple lenders, there is often an alternative pathway that allows your purchase to proceed. At Laxmi Home Loans, we have helped many clients navigate difficult valuation outcomes, including complex land and construction loans, whether they were first home buyers or experienced investors.

Ready to Discuss

If your bank valuation has come in lower than expected, do not assume there is no solution. Let us review your situation and explore the home loan options available before you make your next move.

Disclaimer: This article provides general information only and does not constitute financial, legal or credit advice. Lending approval, valuation outcomes and eligibility criteria vary between lenders and depend on your individual circumstances. Mero Chino Groups Pty Ltd trading as Laxmi Home Loans, ABN 76 169 013 012, Credit Representative Number 476974 is authorised under Australian Credit Licence Number 383640.

Nepali Speaking Home Loan Expert Australia | First Home Buyers, Refinance and Investors Nepali Speaking Home Loan Expert Australia: First Home Buyers, Refinance and Investors

Laxmi Home Loans Wins Two Major Awards | Trusted Nepali Mortgage Broker Australia Laxmi Home Loans Home Loans First Home Buyers Refinance Contact Home /