Pre-approval is not final approval. Learn the key differences and how to secure reliable finance before making an offer on your first home.

Pre-approval is a lender’s initial indication of how much they may lend you, based on the information provided at that time, and it is not a guarantee. Final approval, also called unconditional approval, is the lender’s formal commitment to provide the loan after verifying your documents, completing a property valuation, and confirming every condition is met. Many first home buyers treat pre-approval as a done deal and find out the hard way when finance falls through close to settlement. This guide explains the difference and how to move from pre-approval to unconditional approval without a hitch.

Many first home buyers believe pre-approval means their loan is guaranteed. Some discover the difference the hard way, when finance conditions are not met, and a purchase falls through after they have already given notice on their rental, booked removalists, or told family the good news.

This guide covers what pre-approval and final approval actually are, why the distinction matters, the real reasons finance falls over after pre-approval, and the steps that keep your application moving smoothly from one to the other.

What Is Mortgage Pre Approval?

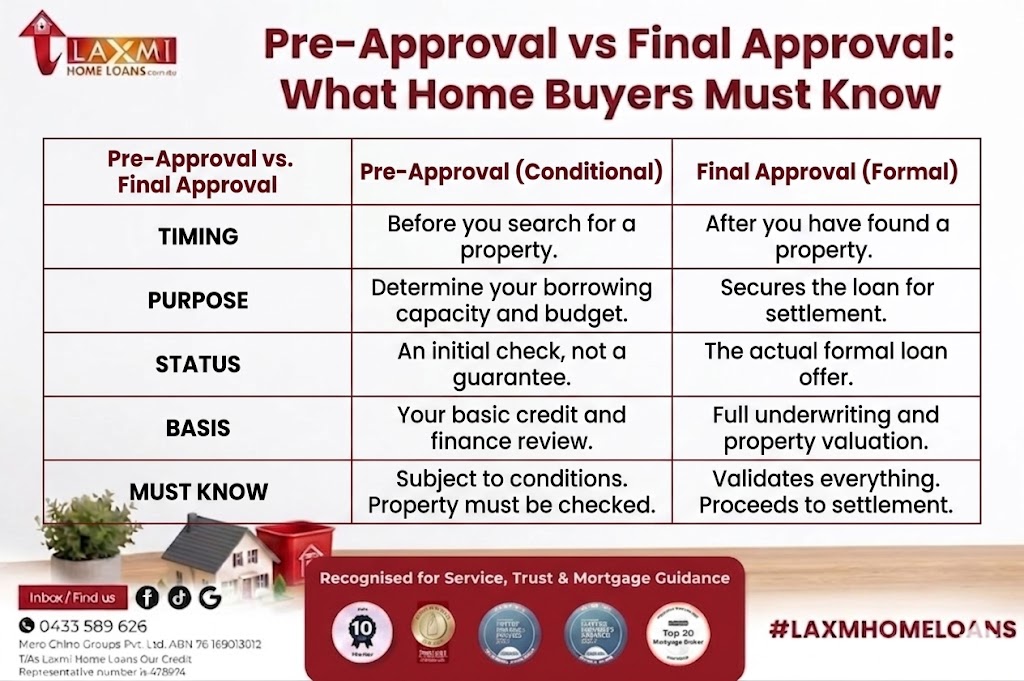

Pre-approval is an initial assessment by a lender indicating how much they are likely to lend you, based on the information you provide at the time. It is valid for a limited period, usually 90 days, though some lenders extend it to longer, and it remains subject to conditions.

Pre-approval is genuinely useful. It confirms your budget before you start inspecting properties, signals to agents that you are a serious buyer, and gives you the confidence to make an offer or bid at auction. Start here with our pre-approval page if you have not yet applied.

What pre-approval is not is a guarantee. The lender has not seen the specific property you intend to buy, has not ordered a valuation, and has not completed full verification of your documents. Everything up to this point is based on what you have told them and a preliminary check.

What Is Final (Unconditional) Approval?

Final approval, also called unconditional approval, is the lender’s formal commitment to provide the loan once every condition has been satisfied. This happens after the lender verifies your payslips, tax returns, bank statements and identification in full, orders and receives a valuation on the specific property you are buying, and confirms there has been no material change to your financial position since pre-approval.

Only at unconditional approval does the lender’s offer become binding, subject to the terms of your loan contract. This is the approval that actually settles your purchase.

Key Differences Between Pre Approval and Final Approval

Pre-approval is based on estimates and preliminary checks using the information you provided, while final approval is based on full verification, a property valuation and legal checks completed by the lender.

The risk profile differs significantly too. Pre-approval can be withdrawn or amended if your circumstances change or the lender’s policy shifts, while final approval is binding subject to your contract terms, which is why settlements rarely fail once unconditional approval has been issued.

In practice, this means pre-approval tells you what you can probably borrow, while final approval tells you what you will definitely receive for this specific property.

The Quick Breakdown: Pre Approval vs Final Approval

| Feature | Pre-Approval (Conditional) | Final Approval (Unconditional) |

| When it happens | Before you start property hunting. | After you find a property and sign a contract. |

| What it means | The bank might lend to you, pending a property check. | The bank will lend to you. |

| Property Specific? | No. | Yes. It is tied to the exact address you are buying. |

| Is it a guarantee? | No. Conditions apply. | Yes. The funds are secured for settlement. |

| Validity Period | Usually 90 days. | Valid up until your settlement date. |

Other Synonyms for Pre-Approval and Unconditional Approval

| Pre-Approval | Unconditional Approval |

|---|---|

| Conditional Approval | Formal Approval |

| Approval in Principle (AIP) | Final Approval |

| Indicative Approval | Full Approval |

| Preliminary Approval | Unconditional Finance Approval |

| Initial Approval | Final Loan Approval |

| Provisional Approval | Loan Approved |

| Finance Pre-Approval | Finance Approved |

| Home Loan Pre-Approval | Home Loan Approved |

| Conditional Finance Approval | Unconditional Finance Approval |

| Borrowing Capacity Approval | Ready to Settle Approval |

| Credit Pre-Approval | Credit Approved |

| Preliminary Finance Approval | Final Credit Approval |

| Lending Pre-Approval | Loan Ready for Settlement |

| Pre-Qualified (not always the same) | Fully Assessed Approval |

| In-Principle Finance Approval | Fully Approved Home Loan |

Why Finance Can Still Fall Over After Pre-Approval

Several things can derail a pre-approved buyer before settlement. A change in employment, even a positive one such as starting a new job, can reset a lender’s serviceability assessment. New debts taken on after pre-approval, including a car loan, an increased credit card limit, or a buy now pay later account, reduce your borrowing capacity at the worst possible time. A property valuation that comes in lower than the purchase price creates a funding shortfall the buyer did not budget for. And issues uncovered during final checks, such as undisclosed rental arrears on an investment property or a strata report flagging building defects, can also stall or stop an approval.

Real-life example. A couple in Sydney received pre approval and found their dream home, only to lose it when the final valuation came in lower than expected, and the gap could not be bridged with their available funds. Working with their broker on a second lender option, one with a different valuer and a policy better suited to their situation, helped them secure another property successfully within weeks. If a low valuation happens to you, our 20 questions to ask your mortgage broker cover exactly this scenario in Q15.

Actionable Steps to Move From Pre-Approval to Final Approval

Provide complete and accurate documentation from the start, since gaps and inconsistencies are the most common cause of delay between pre-approval and final approval. Avoid major financial changes after pre-approval, including new loans, new credit cards, large purchases on existing cards, or changing jobs, until after settlement. Choose properties within your approved valuation range, and if you are unsure where that range sits, our how much can I borrow guide explains how lenders calculate it. Engage a broker who can manage multiple lender options, so if one lender’s valuation or policy creates a problem, a second option is already understood and ready. And stay in regular communication with your broker and lender throughout, because most delays are caught early when someone is actively chasing the file.

3 Critical Mistakes to Avoid Between Pre and Final Approval

Many first home buyers unknowingly sabotage their final approval by making financial changes after they receive pre-approval. Your pre-approval is based on a snapshot of your finances at that exact moment. If that snapshot changes, the bank can pull the plug.

To ensure a smooth transition to final approval, avoid doing the following:

Do not spend your deposit: It sounds obvious, but make sure your saved funds remain exactly where you told the bank they were.

Do not change jobs: Lenders love stability. Switching employers, moving from full-time to casual, or starting your own business can make lenders extremely nervous.

Do not take on new debt: Avoid financing a new car, applying for new credit cards, or using “Buy Now, Pay Later” services. This affects your borrowing capacity.

Key Takeaways

Pre-approval is a helpful guide to your budget, not a guarantee of your loan. Final approval requires full verification of your documents, your finances, and the property itself. Early professional assistance, before you start inspecting properties and again the moment you have a contract, reduces the risk of finance falling over at the worst possible time.

GET IN TOUCH

Ready to check your eligibility and compare lenders?

Frequently Asked Questions

Ready to Take the Next Step?

At Laxmi Home Loans, we guide first home buyers from initial pre-approval through to unconditional final approval with minimal stress. Our experienced team offers no-obligation consultations and expert lender matching for clients across Sydney and Australia.

Book your free consultation today. We make the move from pre-approval to settled home simple and reliable.

Book a Free Appointment with Laxmi Home Loans

Conclusion

Understanding the difference between pre-approval and final approval protects your purchase and gives you confidence at every stage. Partner with a broker who manages the gap between the two, and you reduce the risk of finance falling over when it matters most.

This information is general in nature and does not take into account your personal objectives, financial situation or needs. Lenders assess each application individually and results vary. All loans are subject to lender approval and eligibility criteria. Laxmi Home Loans is the trading name of Mero Chino Groups Pty Ltd, ABN 76 169 013 012, Credit Representative No. 476974 under Australian Credit Licence 383640.